What You Need to Know About Massachusetts’ New Non-Resident Withholding Regulation

Effective November 1, 2025, a new regulation comes into effect in Massachusetts that impacts home sales over $1M.

A Simple Overview

This new regulation ensures Massachusetts collects taxes from sellers before they leave the state. It is not a new tax, but changes when and how the payment is submitted to the Department of Revenue (DOR).

Key Takeaways

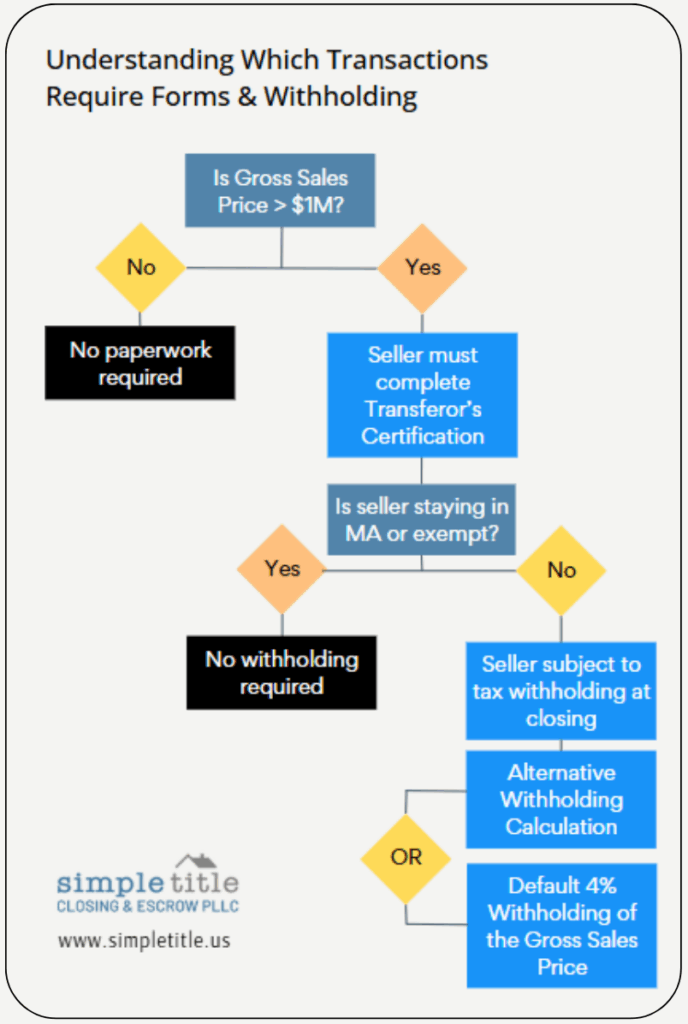

If Gross Sales Price is greater than $1M, two additional forms will be required regardless of non-resident or exemption status

- Transferor’s Certification – to be completed by EACH seller prior to closing. Through this form the seller declares if they qualify for exemptions or reductions and their preferred withholding calculation method. If your seller is a trust, each beneficiary will be required to submit their own certification.

- Non-Resident Withholding (NRW) form – to be completed by the closing attorney, title company or escrow agent

Sellers who plan to move out of state after closing (and don’t meet any other exemptions) will be responsible for paying MA state property taxes at closing

- This may affect on-hand cash for any subsequent home purchase or loan

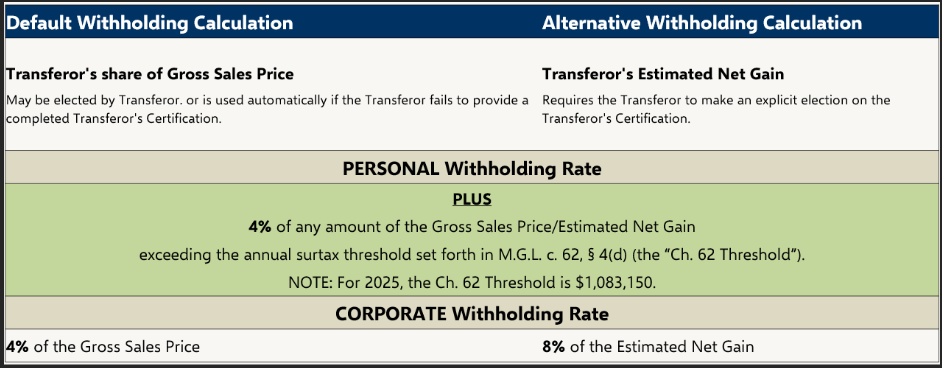

- Sellers can choose between default or alternative tax withholding methods and may want a tax professional to assist with the Transferor’s Certification calculations.

Filing and any withholding must be filed by the closing attorney within 10 days of closing

Tax Withholding Exemptions

Full-year Residents

- Individuals who have resided in the Commonwealth from January 1 in the year the closing is occurring, and who certify they will continue to reside in the Commonwealth post-closing

Pass-through Entities (But Not Disregarded Entities)

- An entity whose income flows through to members for MA tax purposes.

- NOTE: Disregarded entities, such as grantor trusts or single-member LLCs are not considered pass-through entities.

An estate of a resident decedent or a resident trust As defined in M.G.L. c. 62, § 10(c)

Corporate and Organizational Exemptions

- Nonprofits qualified under Code sec. 501 and exempt from tax in MA;

- Certain insurance companies;

- Financial institutions which Maintains a Place of Business in MA;

- FNMA, FHLMC, GNMA, and private mortgage insurance companies;

- Publicly traded partnerships;

- Corporations with a Continuing MA Business Presence, which:

- Represent that it will file a MA tax return for the current year, AND

- Is not selling all or substantially all of its assets in MA.

Reduced or Eliminated Withholding Scenarios

Non-Recognition (Reduction of Withholding Scenarios)

When the gain is not fully recognized for tax purposes, withholding may be reduced or eliminated. Examples:

- Sale of a principal residence

- Transfer to a spouse pursuant to a divorce

- Tax-free reorganizations and 1031 exchanges

- Installment Sales (reduced based on the amount of deferred consideration)

Insufficient Proceeds (Seller is Upside Down)

The withholding amount is limited to the net proceeds available to the Transferor after paying off debts secured by the property at closing. NOTE: Debts do NOT include amounts incurred in contemplation of the Transfer and/or secured less than 90 days prior to closing.

Close with Simple Title. Close with confidence.

Close with the team that keeps you informed.

(978) 539-7500 | info@simpletitle.us

Convenient locations in MA, NH, ME, CT, RI & FL. Expert assistance in English, Spanish and Greek.

NOTE: The materials and information contained herein are provided for informational purposes only and do not constitute legal or tax advice. You should consult with your own legal or tax advisors before taking any action based on the content of this article.

Contact Us

"*" indicates required fields